The key trends that are likely to impact global supply-chains for critical minerals in 2024.

1. Gigafactories make demand estimates concrete

In 2024, after a few years of significant investment, many battery gigafactories – those with massive storage capacity - will become operational. According to Benchmark Minerals, annual investments in these facilities went from less than USD 30bn in 2019 to more than USD 130bn in 2022. Mostly a result of the growing momentum for EVs, this will remain a key aspect of the energy transition in many regions, including the US, China and Europe. Battery gigafactories will play a key role in defining market dynamics in the critical minerals space – for mining companies and other players across the supply-chain - with 2024 representing an important milestone for such a trend.

The mining sector has, so far, been reasonably responsive to such increased demand prospects. Investments in new and existing mines have increased around the world in the past years, despite short-term price fluctuations. However, supply-resilience has yet to be tested. In addition to meeting unprecedented quantity requirements, markets will need to adjust to localisation trends, technology advancements and security concerns. The strategic nature of critical minerals means that such operational challenges will also become political, exposing businesses to increasingly complex regulatory and reputational risks in 2024.

2. Trade controls go global

The fact that many of these new factories – particularly in the US and Europe - benefit from incentives from industrial policies means that they need to comply with geopolitics-driven sourcing requirements. In the concrete sector, this means reducing dependence on China – which, in turn, means adding fuel to the competition fire. In 2024, countries such as Australia and Brazil will likely introduce their own industrial policies, reinforcing a trend that was mainly set by the US Inflation Reduction Act. While 2022-2023 saw the Chinese government showcasing its supply-chain dominance with symbolic and reduced-impact trade controls for certain minerals, 2024 will likely see geopolitical priorities weighing in on the implementation of such controls.

As well as US-China geopolitical competition, trade controls will also be driven by economic verticalisation attempts. Notably, countries in Africa and Latin America - such as DR Congo, Nigeria and Chile - will likely strengthen conditions for producing companies to export critical minerals in an attempt to boost their domestic processing capacity. They will likely mirror, to some extent, Indonesia, which managed to attract different automakers to its domestic manufacturing market by establishing a combination of trade controls with pragmatic geopolitical action.

Read more on investing in critical minerals here.

3. Producing countries face maturity test

The countries holding high minerals reserves can have a significantly different perspective to those already producing on a large scale. In the past few years, much political attention has been centred on countries that sit on large reserves and might eventually become leaders in mineral production. As demand manifests, it is time for consumer players to rely on suppliers who are able to translate reserves into deliveries.

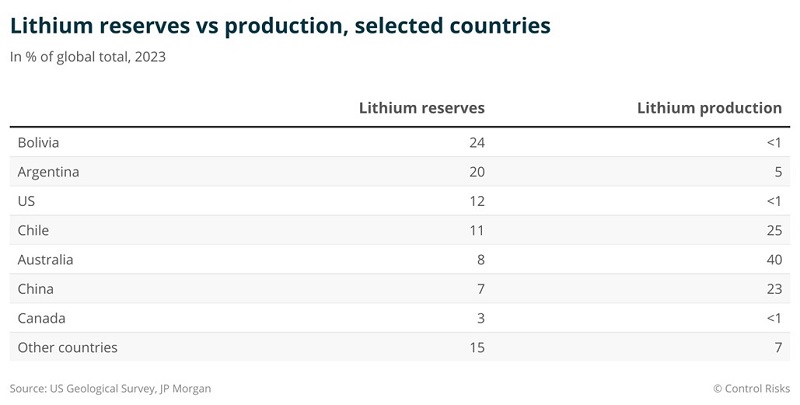

Latin America is a notable case of how complex this can be. Although Bolivia and Chile hold some of the world’s largest (known) lithium reserves, the first presents significant infrastructure challenges for production, while the latter shows significant regulatory uncertainty. Looking ahead, neighbouring countries with less impressive reserves but more mature producing credentials – such as Argentina and even Brazil - might become the ultimate production winners regionally, underlining the power of short-term pragmatism over long-term hesitation. Globally speaking, mining-champion Australia, which holds 8% of the world’s reserves but 40% of production, will be the one to catch.

4. Technology disruptions shape new trends

December 2023 saw the world’s tallest wooden turbine start turning in Sweden. Not only is the technology almost minerals-free, but it is also carbon negative, representing an impressive (even if early-stage) disruption in the wind energy sector. Although anecdotal, this example underlines the increased incentives for technology developments posed by the energy transition rush, becoming increasingly clear in 2024.

Innovation – even if incremental - will be a key aspect impacting the critical minerals space in 2024, on both the demand and supply side of things. Batteries recycling mechanisms, specifically, will be in the spotlight, as companies and governments increasingly see them as an alternative to the geopolitical, operational and sustainability challenges related to the sourcing of critical minerals.

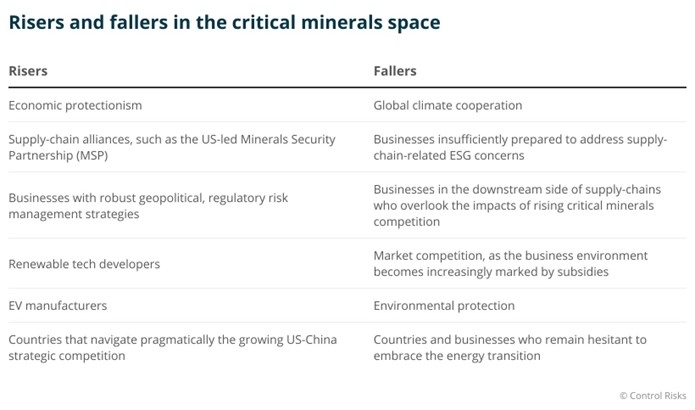

5. Risers and fallers

Like many other aspects of the energy transition, the critical minerals race will produce winners and losers. Countries will be defined by different and interconnected phenomena, including natural reserves, regulatory maturity and geopolitical positioning. Countries like Australia, Canada, Argentina and Indonesia are currently well positioned (if for different reasons) to become interesting success stories.

From a business perspective, winners will be companies and investors who are proactive regarding geopolitical and ESG trends and adopt an agnostic view about the far-reaching impacts – including supply-chains – of critical minerals competition. Those with technical expertise gained in other activities that can be adapted to critical minerals will also be potential champions – a good example being that of companies with oil and gas offshore expertise who are willing to take risks in the seabed mining world.